Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Comparing Home Loans

Comparing Home Loans: How to Choose the Right Mortgage in 2026

Comparing home loans is one of the most important steps in the home buying process, especially in a competitive market like Coeur d’Alene and Kootenai County. Many buyers focus only on interest rates, but the reality is that the best loan depends on your total monthly payment, upfront costs, loan structure, and how long you plan to stay in the home.

Whether you are buying your first home, relocating to North Idaho, or upgrading into a new property, understanding how to compare loan options properly can save you thousands of dollars over time and help you make stronger offers when you find the right home.

Before choosing a loan, it’s helpful to review your overall strategy: First-Time Homebuyer Tips, Current Market Conditions, and Relocating to Coeur d’Alene.

What to Compare When Looking at Home Loans

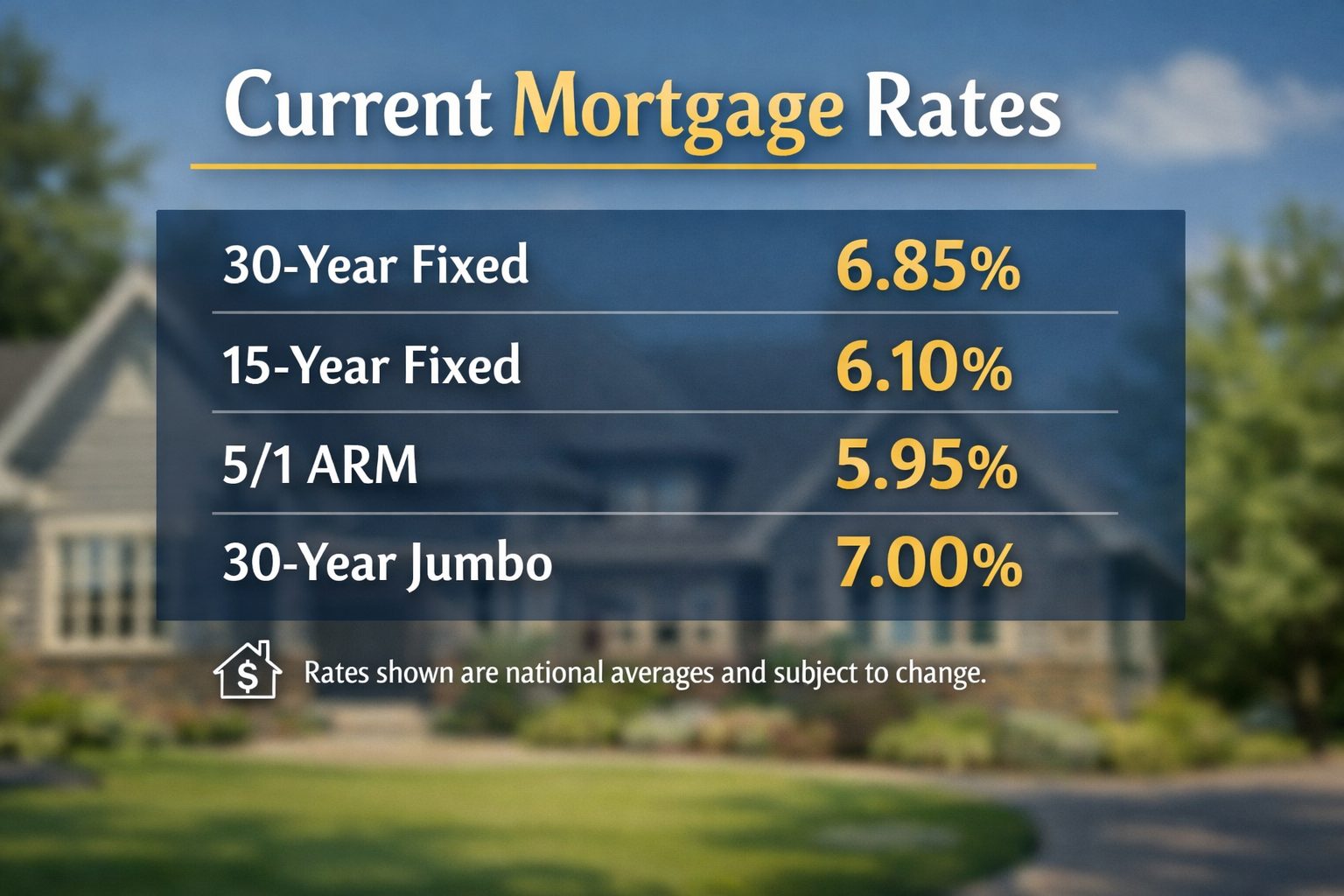

When comparing mortgage options, you need to look beyond just the advertised interest rate. Two loans with similar rates can have very different costs depending on fees, mortgage insurance, and structure.

Here’s what actually matters when comparing loan offers:

- Interest Rate vs APR: The interest rate determines your monthly payment, while APR includes certain loan costs. APR gives you a broader view, but it still doesn’t tell the full story on cash to close or long-term flexibility.

- Monthly Payment: Focus on your total housing payment, including principal, interest, taxes, insurance, and mortgage insurance. This is what impacts your monthly budget.

- Cash to Close: This includes your down payment plus closing costs. Some loans require significantly more upfront cash than others.

- Mortgage Insurance: Some loans require ongoing insurance (FHA, low-down-payment conventional), while others (like VA) may not. This can have a major impact on long-term cost.

- Loan Flexibility: Some loans allow you to remove mortgage insurance later, refinance more easily, or work with a wider range of property types.

Why Loan Estimates Matter More Than Rate Quotes

Many buyers make the mistake of comparing lenders based on quick rate quotes. The better approach is to request multiple Loan Estimates, which standardize how lenders present costs.

A Loan Estimate allows you to compare:

- True monthly payment: Including mortgage insurance and escrow estimates.

- Total closing costs: Lender fees, title costs, prepaid expenses, and more.

- Points vs lender credits: Whether you are paying upfront to lower your rate or receiving credits to reduce closing costs.

- Cash required at closing: One of the biggest decision factors for many buyers.

Always make sure you are comparing the same loan type, similar rate lock timing, and similar assumptions when reviewing estimates. Otherwise, one lender may appear cheaper when it is actually structured differently.

Detailed Breakdown of Common Loan Types

Conventional Loans

Conventional loans are one of the most common choices for buyers with strong credit profiles. They offer flexibility and are widely accepted across different property types, including primary homes, second homes, and some investment properties.

One major advantage of conventional loans is that mortgage insurance can often be removed once you reach sufficient equity. This makes them attractive for buyers who plan to stay in the home long enough to benefit from lower long-term costs.

These loans are typically best suited for buyers who have stable income, solid credit, and some funds available for down payment and closing costs.

FHA Loans

FHA loans are designed to make homeownership more accessible, especially for first-time buyers or those with more limited savings. They allow lower down payments and can be more flexible with credit requirements compared to conventional financing.

However, FHA loans include mortgage insurance that typically lasts for the life of the loan unless refinanced. That makes it important to compare FHA options against conventional programs if you expect your financial profile to improve over time.

VA Loans

VA loans are one of the most powerful financing tools available to eligible military buyers. These loans often allow little or no down payment and do not require monthly private mortgage insurance, which can significantly reduce monthly costs.

In competitive markets like Coeur d’Alene, a strong VA pre-approval can also make your offer more attractive when paired with the right strategy.

USDA Loans

USDA loans are designed for eligible rural and semi-rural areas, which can include parts of North Idaho outside the immediate city core. These loans can provide low upfront cost options for buyers who meet income and property eligibility guidelines.

They are often overlooked but can be a strong option for buyers willing to explore areas outside central Coeur d’Alene.

HomeReady and Home Possible

These are low down payment conventional programs that can compete directly with FHA loans. For qualified buyers, they may offer lower long-term costs while still requiring relatively little upfront cash.

They are especially useful for buyers who want to stay within the conventional loan category but need flexibility on down payment.

How Financing Impacts Your Home Search in Kootenai County

Your loan choice directly affects what homes you can realistically pursue. Some properties may be easier to finance than others depending on condition, location, and loan type requirements.

For example, homes in certain price ranges or conditions may align better with conventional financing, while others may require more flexibility depending on appraisal or property standards.

To better understand what fits your budget and lifestyle, explore: Kootenai County Cities & Communities Guide

Smart Strategies for Comparing Home Loans

Comparing loans effectively is not just about numbers — it’s about aligning your financing with your goals and timeline.

- Compare multiple lenders: This gives you leverage and helps identify the best structure.

- Focus on total cost: Monthly payment + upfront cash matters more than rate alone.

- Understand your timeline: The longer you stay, the more long-term cost matters.

- Ask about flexibility: Can you refinance? Remove PMI? Adjust later?

- Work with a strong local team: Financing and home strategy should work together.

Need Help Comparing Loan Options in North Idaho?

Choosing the right loan is only part of the equation. Understanding what that loan allows you to buy in Coeur d’Alene and Kootenai County is just as important.

Call or text: 208-699-5676

Email: david.puccetti@cbinw.com

Contact David Puccetti for personalized guidance.

Frequently Asked Questions

What is the most important factor when comparing home loans?

The total cost of the loan, including monthly payment, upfront cash, and long-term expenses.

Is the lowest rate always the best option?

No. Lower rates can come with higher upfront costs or less flexibility.

Should I compare multiple lenders?

Yes. This gives you better insight and negotiating power.